Country risk premium is defined as the additional return demanded by investors to invest in a specific country asset beyond the return on a similarly liquid and risk-free asset (e.g. US or German government bonds) denominated in the same currency, having similar transaction costs and maturity. It not only reflects the government borrowing costs but also serves as a benchmark for external borrowing terms and costs of domestic financial institutions, firms, and households. In this respect, understanding the drivers of country risk premium and the interaction of these variables with the global risk appetite is important for policymakers.

Country risk premium may be affected by global factors and country-specific macroeconomic indicators. For example, it is known that a decrease in the global risk appetite exerts an upward pressure on country risk premiums of emerging market economies (EMEs). On the other hand, country-specific factors such as the current account balance, international reserves, fiscal balance, private sector indebtedness, and growth may also affect the risk premium. In this blog post, we analyze whether the country-specific macroeconomic indicators gain further importance in periods when the global risk appetite deteriorates.

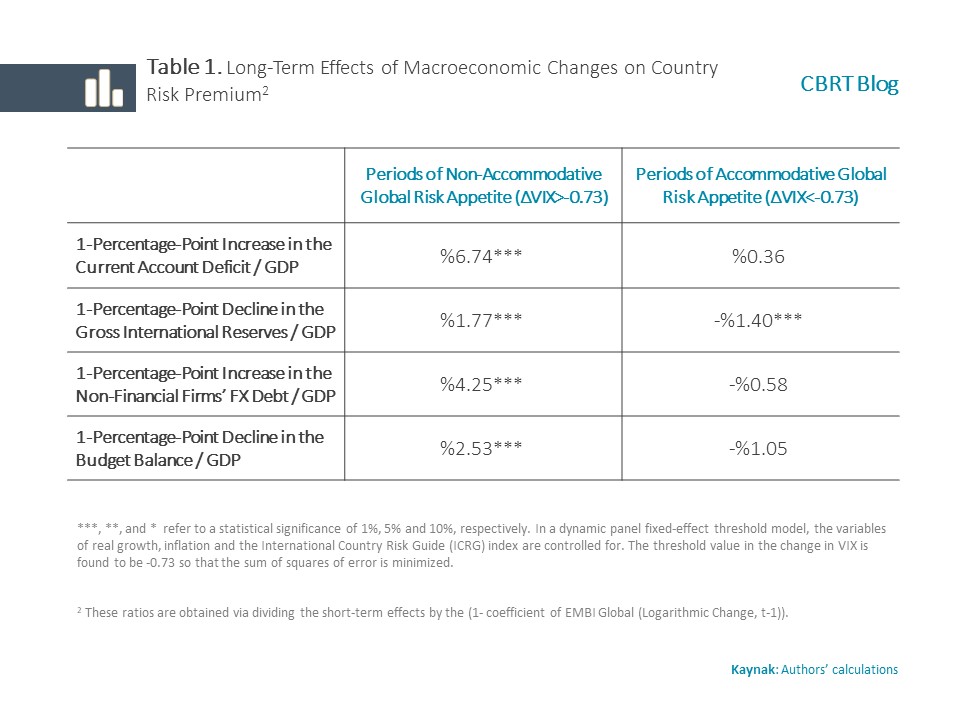

This study examines the drivers of country risk premiums for seven major emerging economies: Brazil, Indonesia, South Africa, Colombia, Malaysia, Mexico, and Turkey. The JP Morgan EMBI Global index that consists of government bonds issued by EMEs is used as a risk premium. The sample period is 2005Q1-2017Q4.[1]

Table 1 demonstrates the results of the analysis. The VIX index is used as a global risk appetite indicator. A 1-percentage-point deterioration in the current account balance raises the country risk premium by 6.74% when the global risk appetite is not accommodative, whereas it has no significant impact when the global risk appetite is accommodative. Similarly, a decrease in international reserves leads to an effect on country risk premium particularly when the global risk appetite is not accommodative. A 1-percentage-point increase in FX indebtedness of non-financial firms pushes up the country risk premium by 4.25% in periods of non-accommodative global risk appetite. On the other hand, FX indebtedness of firms is found to have no significant effect on country risk premium in periods when the global risk appetite is accommodative. Finally, a 1 percentage-point deterioration in the public budget balance/GDP ratio has no significant effect on the country risk premium when the global risk appetite is accommodative, whereas it increases the country risk premium by 2.53% when the global risk appetite is not accommodative.

To sum up, our empirical analyses show that macroeconomic fundamentals become more important for country risk premium for emerging economies particularly when the global risk appetite is not accommodative.

[1] The dynamic panel bias-corrected fixed-effect threshold model has been used. Variations of error terms have been corrected by using the dynamic system generalized method of moments (system GMM). For details of the method, see Akçelik and Fendoğlu (2019).

References

Akçelik, F. and Fendoğlu, S. (2019). “Country Risk Premium and Macroeconomic Indicators When Global Financial Conditions Slide”, CBRT Research Notes in Economics, 19/04.