Understanding the components of local currency bond yields is crucial for the deepening of debt markets and the reduction of borrowing costs in emerging market economies (EMEs) where a significant portion of the government debt is composed of local currency bonds. In these countries, the currency risk premium is one of the most important determinants of local currency-denominated sovereign bond yields (Domowitz et al. (1998)). The currency risk premium can be basically defined as the extra yield demanded to cover the risk of depreciation in local currency against reserve currencies (Du et al. (2013)). Investors who want to hold local currency-denominated sovereign bonds ask for the rate on US Treasury bonds, an investment instrument that is deemed risk-free, and the credit risk premium that reflects the country’s default risk, in addition to the currency risk premium that they demand in return for a possible depreciation of the local currency against reserve currencies. In this regard, a country’s local currency sovereign bond yield can be decomposed into three components having the same maturity: the US treasury bond yield, the credit risk premium, and the currency risk premium (1). Based on this definition consistent with the academic literature, the currency risk premium (CRP) can be expressed as the residual obtained by excluding the US bond yield rus and credit default swap premium (CDS) from the local currency bond yield for a country (rd):

This blog post explores the course of the currency risk premium embedded in bond yields for emerging market countries as well as the macroeconomic and global factors that may lead to variations in the currency risk premium across these countries (2).

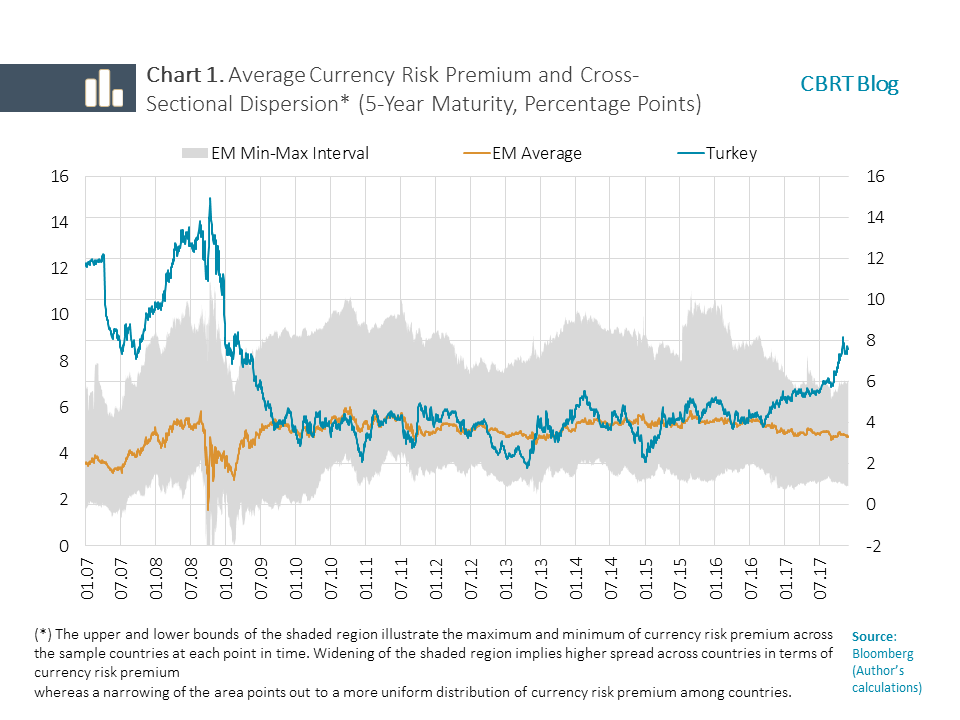

Chart 1 demonstrates the variation in currency risk premia of selected eight emerging market countries obtained for the period between 2007 and 2017 using daily data (3). Currency risk premia fluctuate throughout the analysis period and also significantly vary across countries. The grey area showing the maximum and minimum currency risk premium values for the related period in EMEs excluding Turkey implies that currency risk premium differs across periods while the currency risk premium of Turkey occasionally diverges from the risk premia of other EMEs. In fact, Turkey’s risk premium has displayed an upward trend since 2017 whereas the average of peer countries’ risk premia has been relatively stable.

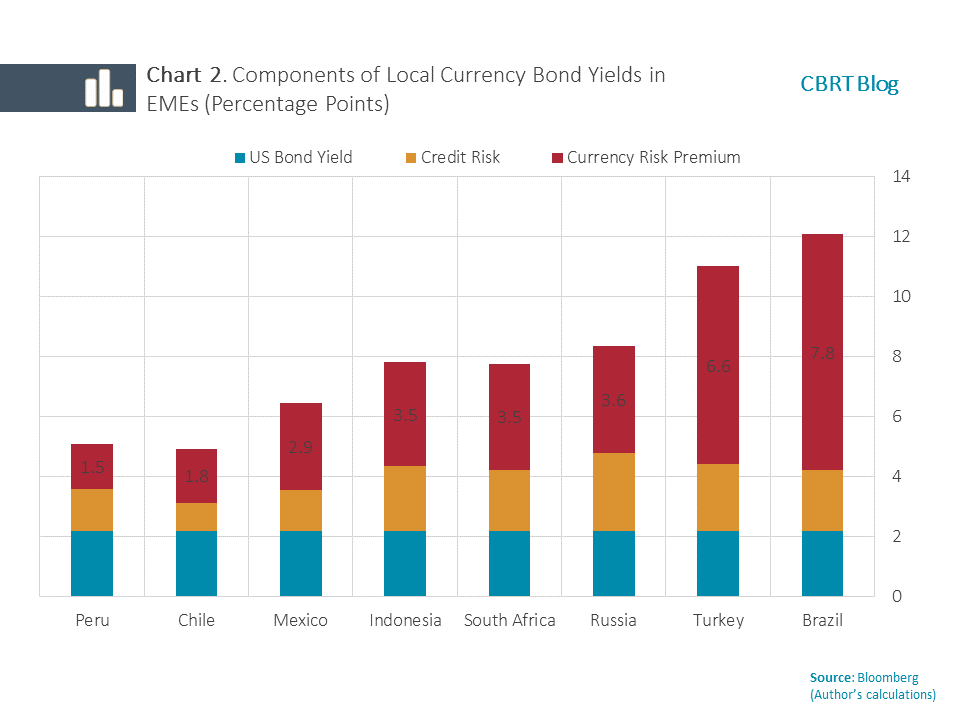

Average annual bond yields in sample countries are decomposed into the currency risk premium and other factors (US bond yield and credit risk) to reveal the role of the currency risk premium in the course of EMEs’ local currency bond yields (Chart 2). For the period between 2007 and 2017, the currency risk premium accounts for 3.9 percentage points of the average local currency bond yield of 7.9% in EMEs while the remaining 4 percentage points are associated with the US bond yield and the sovereign credit risk. For the case in Turkey, 6.6 percentage points of the average Turkish lira bond yield, which was 11% during the same period, are attributed to the currency risk premium and 4.4 percentage points to other factors (4). In other words, for the analysis period, the currency risk premium accounts for almost half of the average EME yield whereas it corresponds to three fifths of the yield in Turkey.

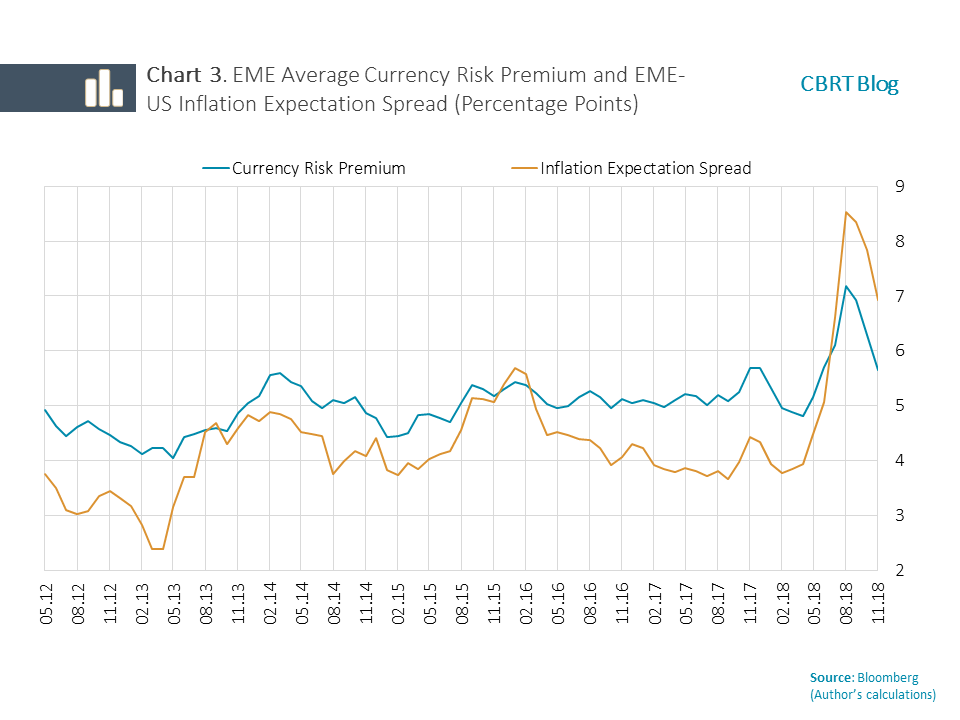

Under the methodology employed to decompose bond yields into their components, the currency risk premium obtained by adjusting the average bond yield spread between EMEs and the US for EMEs’ credit risk is expected to smooth out the real interest rate spreads among countries and the remaining series to largely reflect the cross-country inflation expectation spreads. As a matter of fact, for the EME group, there is a significantly strong relationship between the average currency risk premium and the EME-US inflation expectation spread (Chart 3). This relationship reveals that the factors affecting the currency risk premium in selected EMEs shape bond yields mostly through the channel of inflation expectations (5).

Results indicate that stock variables such as the NIIP and public debt stock play a more important role in the determination of currency risk premium than flow variables such as current account balance and budget balance. On the other hand, it is notable that inflation and growth volatilities are found to be more significant compared to inflation and growth rates. These variables are deemed to be important in terms of explaining the cross-country variations in macroeconomic uncertainty. It is observed that average annual inflation rates become significant but the performance of the model drops when the volatility variables are excluded from the model.

When the results for the determinants of currency risk premium in EMEs are analyzed in terms of policy makers, it is assessed that monetary and fiscal policies addressing price stability and economic rebalancing will positively affect the functioning of debt markets through the currency risk premium channel. Improvements in macroeconomic vulnerability indicators such as public debt stock sustainability, NIIP and international reserves are crucial to control inflation expectations that are susceptible to these factors and also to reduce the sensitivity of currency risk premium to these variables.

References

Korkmaz and Onay, 2018, The Determinants of Currency Risk Premium in Emerging Market Countries, CBRT Research Notes in Economics, 18/06.

Domowitz, I., J. Glen, and A. Madhavan, 1998, Country and Currency Risk Premia in an Emerging Market, The Journal of Financial and Quantitative Analysis, 33 (2): 189-216.

Du, W. and J. Schreger, 2016, Local Currency Sovereign Risk, The Journal of Finance, 71(3): 1027-1070.

IMF, 2016, Development of Local Currency Bond Markets, IMF Staff Note for G20 IFAWG.