The steps taken to encourage Turkish lira deposits are closely related to the relative return on TL deposits against FX-protected deposits (KKM). The KKM provides investors with an option to compensate the realized depreciation of the Turkish lira, in addition to standard TL deposits. This blog post discusses the option value of the KKM as well as the factors determining savers’ preferences between the KKM and TL deposits. It also presents an evaluation of the impact of the CBRT’s steps to strengthen TL deposits from an investor perspective, and reveals that increasing the relative attractiveness of TL deposits has stimulated a decline in KKM balances.

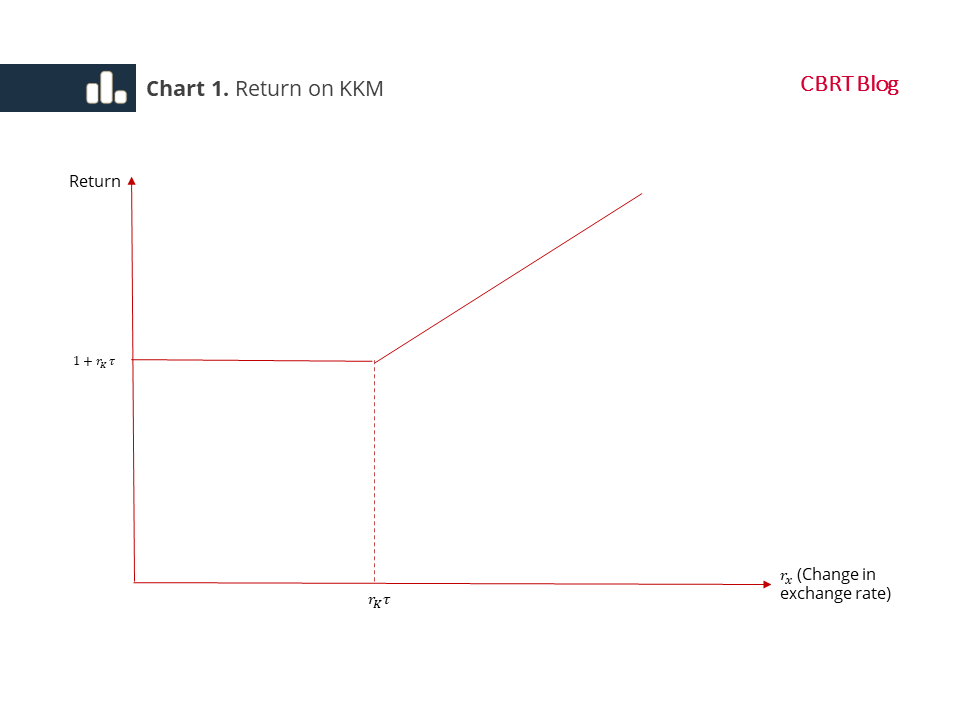

When investors invest their savings in TL deposits, the principal earns interest at TL deposit rates. On the other hand, when the KKM is preferred, the KKM interest rate determines the minimum return but the actual returns depend on the exchange rate. The return on the KKM at maturity is equal to the KKM interest rate if the depreciation of the exchange rate is less than the KKM interest rate, and equal to the change in the exchange rate if the depreciation exceeds the KKM interest rate. Chart 1 shows the cumulative amount of a depositor's 1 Turkish lira principal at maturity in two possible cases.[1]

The return on KKM at maturity can be illustrated as follows:

max{X

The first term indicates the payoff of a time deposit, while the second term indicates an FX call option with the strike price equals to this payoff. Accordingly, a KKM choice offers a call option as well as a time deposit for its investor. For an investor to be indifferent between the KKM and TL deposits, the expected return of both products at the opening of the deposits should be equal.

TL deposit rate=KKM rate+Option price

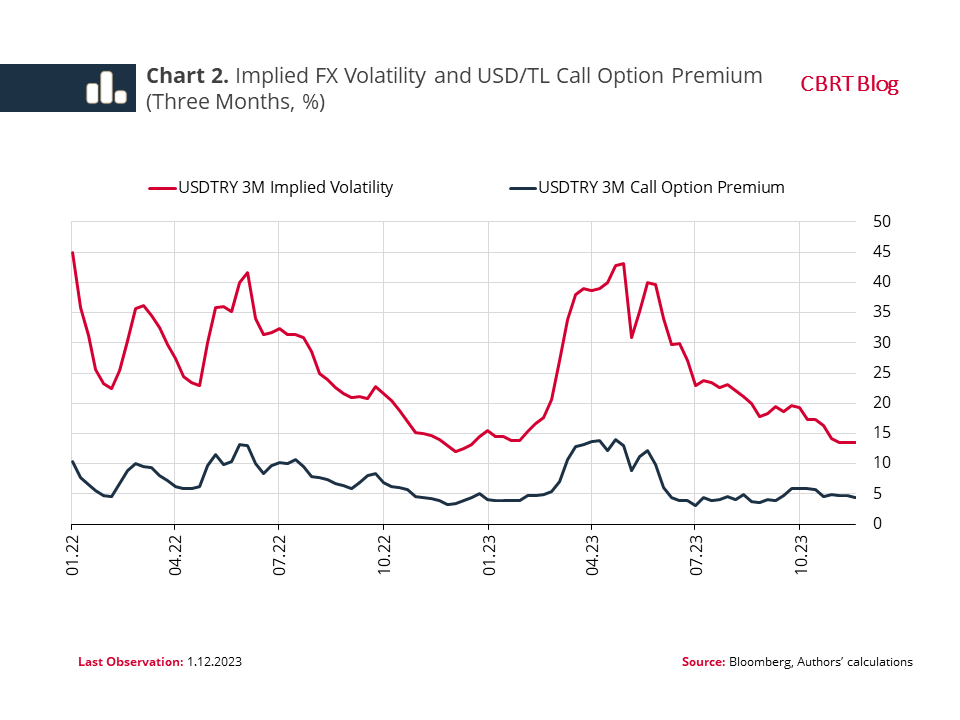

Accordingly, in order for investors to switch from the KKM to TL deposits, the TL deposit rate should be higher than the sum of KKM rate and the option price. Therefore, developments that lead to a lower option price or wider rate spreads increase the relative attractiveness of TL deposits. The option price is affected by the strike price determined by the KKM rate, and the exchange rate volatility shaped by exchange rate expectations.

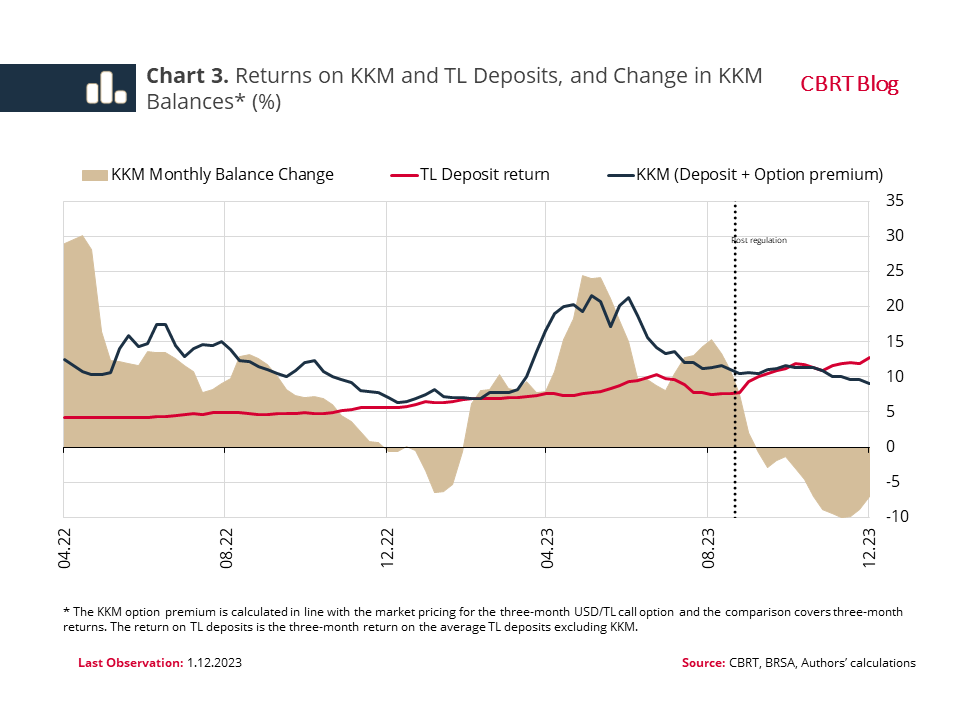

Recent regulations to encourage shift to TL deposits are closely related to the price of the option offered by the KKM and interest rate spreads. Determined policy steps have reduced the exchange rate volatility, and hence the option price (Chart 2). Second, monetary tightening increases the attractiveness of TL deposits. Finally, subsequent macroprudential steps provide banks more flexibility in determining the interest rate spread, while concurrently incentivizing them to raise the TL deposit rate. Thus, by widening the interest rate spread in favor of TL deposits, a gradual shift to TL deposits is being supported (Chart 3).

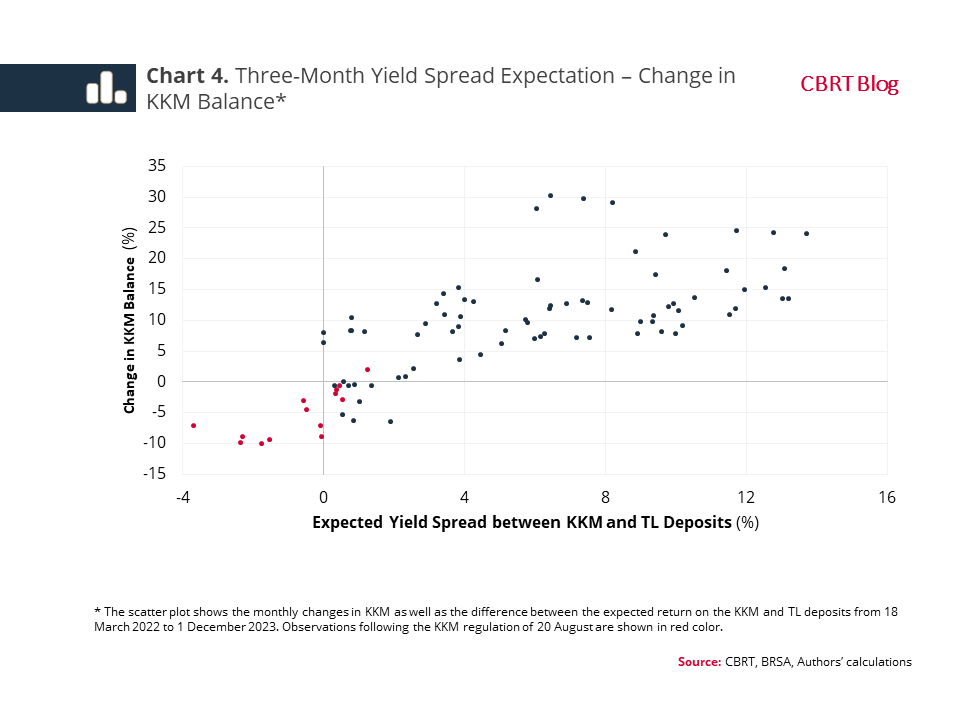

In sum, investors' deposit preferences are shaped by the relative returns on KKM and TL deposits. Higher relative returns on TL deposits as a result of the policy steps taken by the CBRT leads to lower renewals of KKM deposits and lower KKM balances at maturity. The relative yield spread moves in tandem with the change in balances, which reveals the importance of relative returns from an investor’s perspective (Chart 4).

[1] In this blog post,