Macroprudential policies are tools that are complementary to conventional macroeconomic policies and used to contain or prevent likely systemic financial risks. The main objective of these policies is to ensure interrupted provision of basic financial services in the face of domestic and external shocks to an economy and limit their impact on the real economy[1].

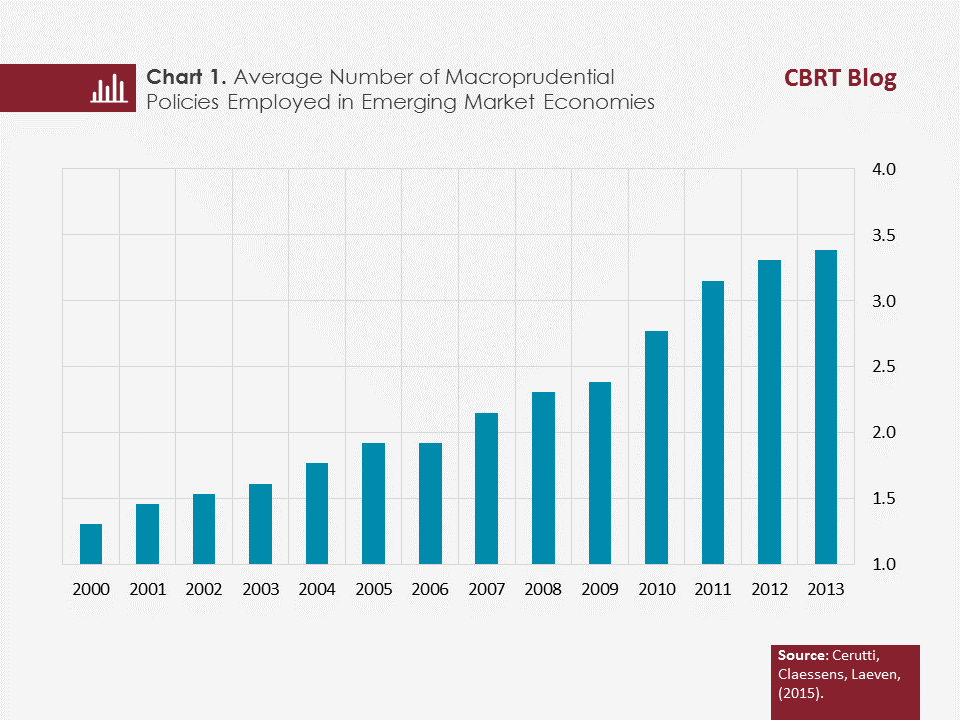

The term “macroprudential policy”[2] first appeared during the 1980s but these policy tools have been used since the Great Depression years of the 1930s[3]. Macroprudential policies have become widespread in both advanced and emerging market economies in the aftermath of the 2008 global financial crisis (GFC) (Chart 1)[4]. The volatility in capital flows increased in the post-GFC period, causing difficulties in managing their impact and devising the appropriate monetary policy, particularly in emerging market economies. The quantitative easing policies of advanced economies increased the capital inflows to emerging market economies, which underlined the need to adopt a macro approach that safeguards financial stability. Large capital inflows led to an appreciation of domestic currencies and acceleration of credit growth[5]. Recently, uncertainties regarding the monetary policies of advanced economies have also been adding to the volatility in capital flows.

The objectives of macroprudential policies in the aftermath of the GFC can be listed as: (i) sustaining credit flows in the economy by mitigating the impact of systemic shocks, (ii) weakening the relationship between credit cycles and asset price cycles, (iii) containing financial vulnerabilities by cutting down on funding from unsustainable resources, and (iv) controlling vulnerabilities by reducing the interconnectedness of the financial system[6].

In this framework, active use of reserve requirement ratios for domestic and foreign currency deposits to keep credit growth under control is one of the macroprudential policies employed in emerging market economies. As another macroprudential policy aimed at safeguarding financial stability, reserve requirement ratios for short-term external loans are set higher than those for long-term loans to put a cap on short-term external borrowing.

Since macroprudential policy tools were not in wide use before the GFC, either the economics literature lacked any information on the short-term and long-term effects of these policies or there was no consensus on their impact. However, studies conducted in recent years are providing us with more comprehensive information regarding the effects of these policies.

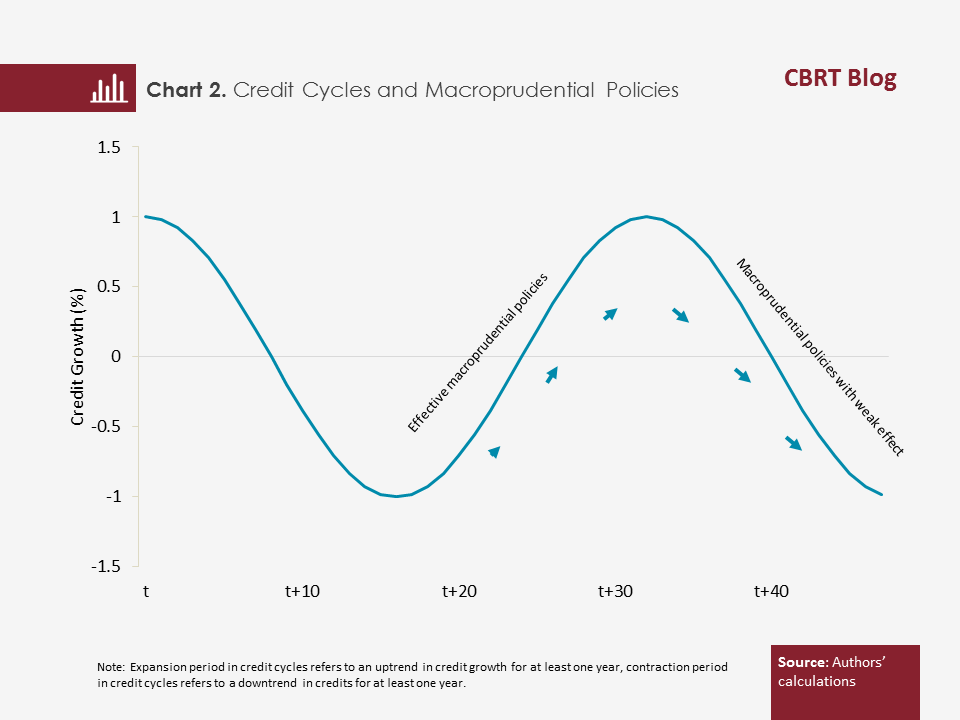

In this blog post, we summarize the results of our study on the circumstances under which the macroprudential policies employed by emerging market economies are effective in containing the credit growth in periods of rising global liquidity[7]. These results have been obtained by using country data of 30 emerging market economies and the panel vector autoregression model. The results demonstrate that credit cycles should be taken into account to assess the effects of macroprudential policies on credit growth. Accordingly, we see that macroprudential policies are effective during periods in which the credit growth rate is above the average whereas they do not have any statistically significant effect during downturns (Chart 2).

The study also tested whether the diversity of macroprudential policies is effective in restraining credit growth. Consequently, we have observed that countries that employ a greater number of macroprudential policies during the same period are better at limiting credit growth. These findings suggest that complementary macroprudential policies can more effectively control credit growth. We can say that these findings are consistent with the “leakage literature”. Accordingly, since individuals or companies take advantage of leakages in the financial system to bypass rules and regulations, complementary macroprudential policies are believed to prevent the formation of such leakages and increase the effectiveness of policies.

To conclude, our findings indicate that the effectiveness of macroprudential policy tools depends on the phase of the credit cycle, i.e. whether credit growth is accelerating or decelerating. Another factor increasing the effectiveness of these policies is that they should be considered as a whole and implemented in line with the pre-defined objective.

[1] “Macroprudential Policy Tools and Frameworks“ Progress Report to G20, October 2011.

[2] Clement, P. «The Term “Macroprudential”: Origins and Evolution», BIS, March 2010.

[3] Brunnnermeier, M. K. and Schnabel, I. (2015) ”Bubbles and Central Banks: Historical Perspectives, CEPR Discussion Papers DP 10528

[4] Cerutti, E., Claessens, S., Laeven, M. L., 2015. "The Use and Effectiveness of Macroprudential Policies: New Evidence", IMF Working Paper No. 15-61.

[5] Kara, H. “A Brief Assessment of Turkey's Macroprudential Policy Approach: 2011-2015”, Central Bank Review, 2016.

[6] CBRT Bulletin Issue: 32, September 2014.

[7] Erdem,P., Özen, E., and Ünalmış, İ (2017), “Are Macroprudential Policies Effective Tools to Reduce Credit Growth in Emerging Markets?”, CBRT Working Paper 17/12.