Inflation expectations play a significant role in inflation dynamics, as they influence multiple channels, including consumption and saving decisions, portfolio preferences, and pricing behaviors. In line with its primary objective of price stability, the Central Bank of the Republic of Türkiye (CBRT) employs the inflation expectations of economic agents as a key input in policy formulation. In this blog post, we examine the role of perceived inflation, prominent items in the consumer basket, and central bank communication in shaping household expectations through a comparative lens of global examples.

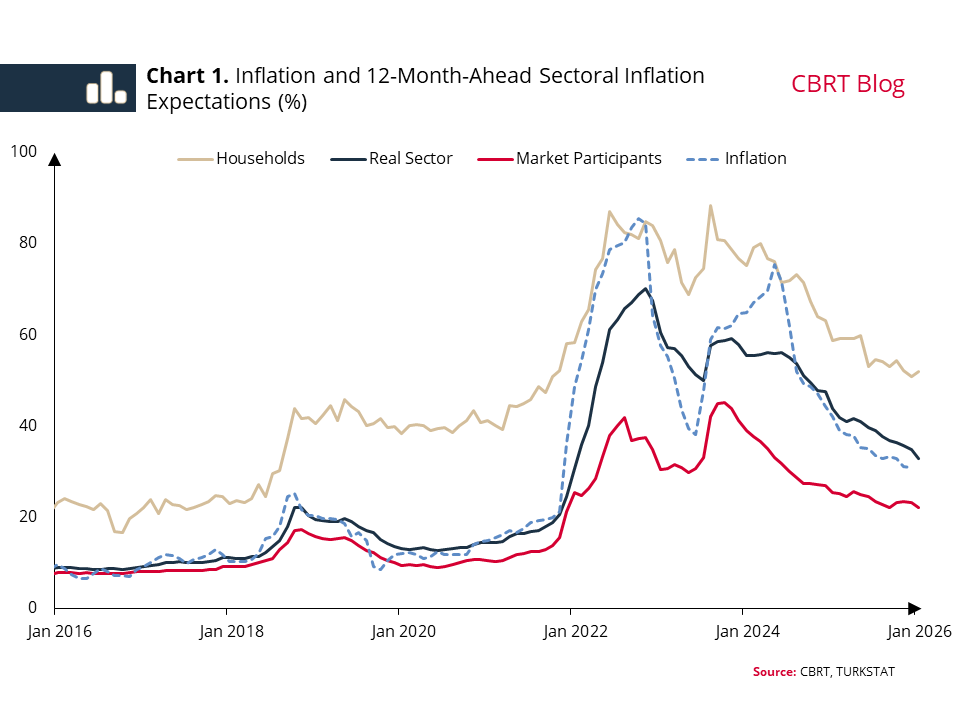

The “Sectoral Inflation Expectations” survey, shared with the public on a monthly basis, covers households and the real sector alongside professional participants. Survey results over the past decade indicate that households’ 12-month-ahead inflation expectations have generally remained well above the actual inflation (Chart 1). This gap is also evident in periods when inflation hovered at single-digit levels. While the real sector’s inflation expectations may fall below or exceed actual inflation, they display a stronger correlation with it. Market participants’ expectations, on the other hand, stand below the headline inflation, reflecting prospects of disinflation. Notably, market participants give the weakest response to volatility in headline inflation.

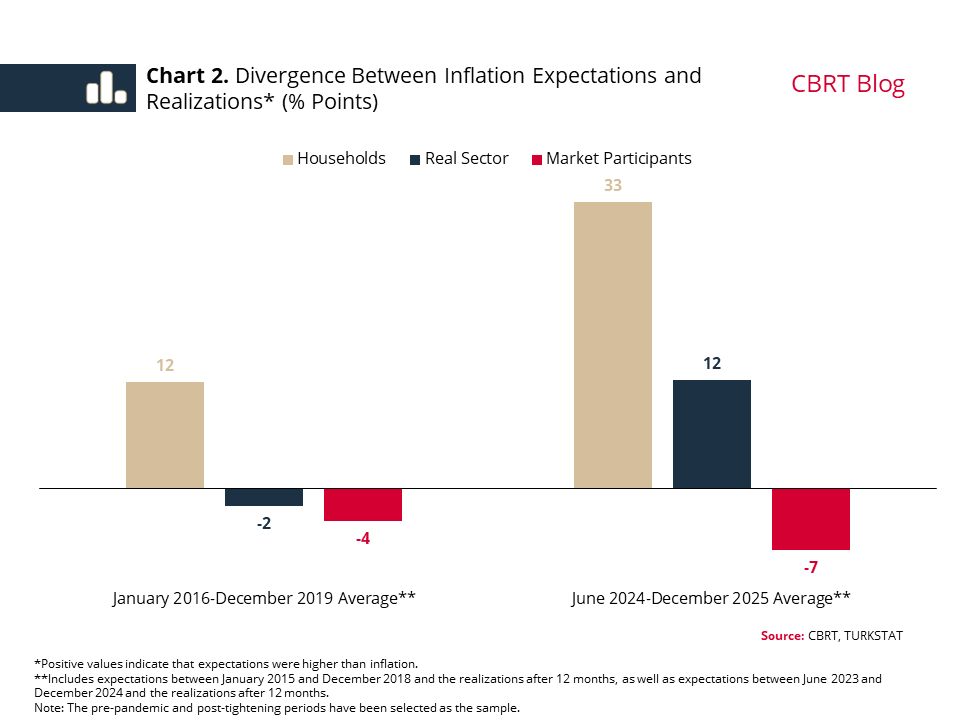

Accordingly, when we examine the predictive power of the 12-month-ahead inflation expectations of each of the three groups, we see that market participants have the lowest margin of error, while households have the highest (Chart 2). Even in years when inflation remains relatively low, household expectations continue to exceed inflation by approximately ten percentage points. In recent years, when inflation has been higher and more volatile, the gap between household expectations and inflation has widened further.

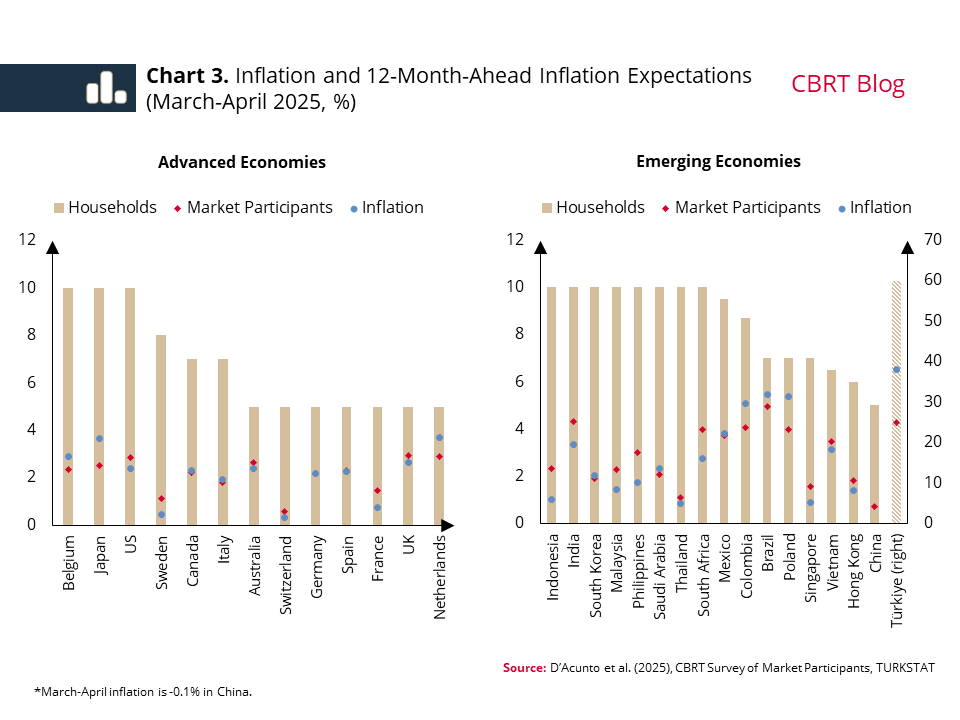

The divergence in inflation expectations among different economic actors — most notably households and market participants — is a phenomenon observed in other countries as well (Chart 3).[1] Household expectations in advanced and emerging economies are observed to be well above actual inflation and professional forecasts. Household expectations, which stand at 10%, are particularly striking in many countries where inflation has remained at 2% or below for a long time.

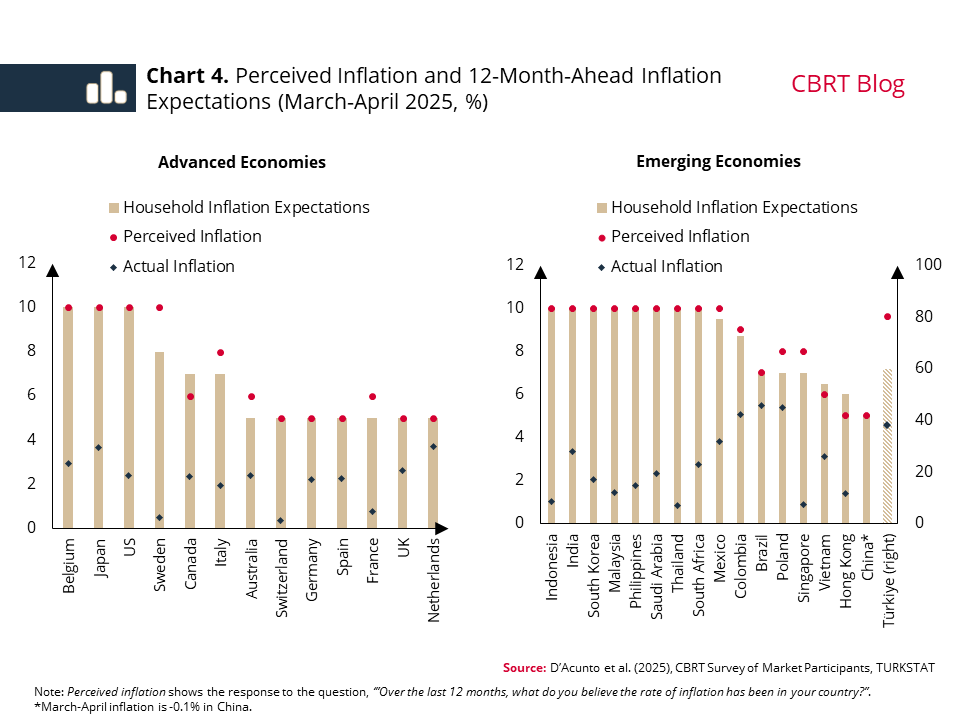

Among the reasons for the aforementioned divergence, perceived inflation stands out in explaining the relatively high course of household expectations.[2] In fact, in advanced and emerging economies perceived inflation and inflation expectations are observed to be at fairly similar levels (Chart 4). This picture reveals that the significant divergence between actual inflation and inflation expectations stems from perceived inflation. The results are also consistent with findings from previous CBRT studies.[3] Another notable point is that despite varying inflation rates, perceived inflation and inflation expectations tend to cluster around round numbers such as 5% and 10%, reflecting a rounding effect.

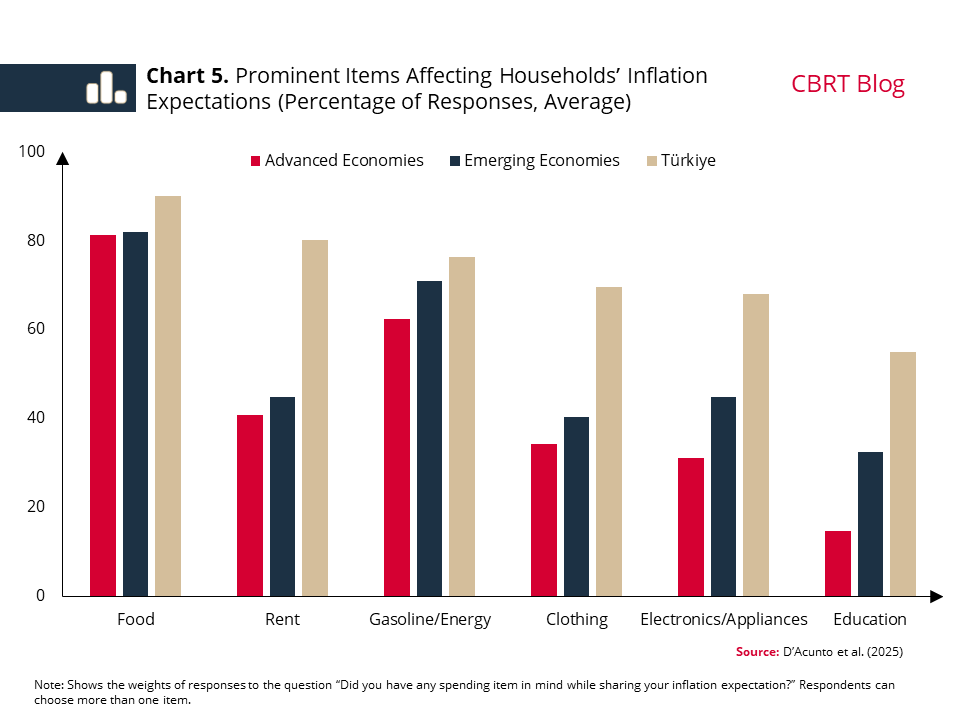

The results show that inflation perceived by households is higher than actual inflation, and reveal that the perceived inflation moves closely with expectations. At this point, examining the factors affecting expectations and perceived inflation is also important. In this regard, we examine data pertaining to the spending items that survey participants take into account when forming their inflation expectations (Chart 5).

Globally, regular expenditure items such as food and energy stand out in households’ inflation expectations. Findings from studies conducted specifically for the European Union also highlight these common factors.[4] In Türkiye, sensitivity to these items is generally even higher. It is also noteworthy that besides food and energy, rents also play a significant role in household expectations. Despite the recent decline, rent inflation, which has been hovering above the headline inflation for a long time, supports this divergence. The results reveal that items such as food, which are frequently consumed and rent, which occupies an important place in the expenditure basket, are important drivers of perceived inflation.

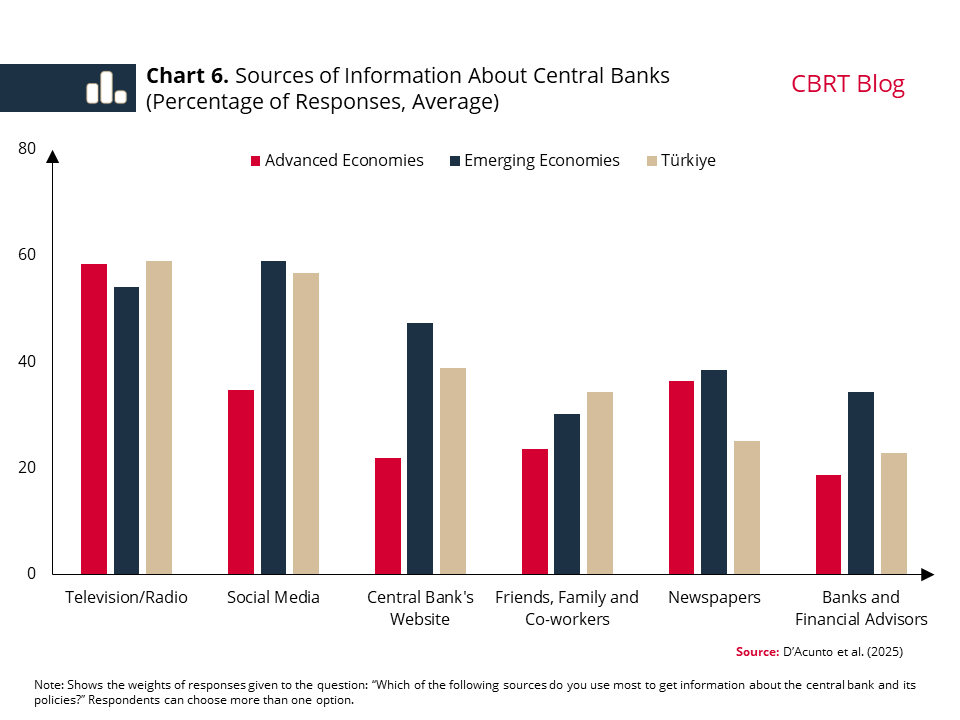

The widening gap between the headline inflation and the price increases in items with the strongest effect on perceived inflation pushes household expectations up. On the other hand, the weakening predictive power of household expectations highlights the importance of effective communication in this area. Indeed, knowledge and awareness about a central bank are known to have a significant relationship with inflation expectations.[5] At this point, households’ information sources about central banks should also be addressed. Similar to other emerging countries, social media is also a powerful source of information in Türkiye, along with television and radio (Chart 6). This reveals the importance of the CBRT’s recent communication through diverse channels for the disinflation process.

To sum up, household inflation expectations structurally remain above the actual inflation and the expectations of other economic actors in Türkiye, as in the rest of the world. The perceived inflation is the underlying reason for this divergence. In Türkiye, rents as well as food and energy stand out as factors that explain the perceived inflation. In this context, the trend of household expectations gains importance alongside their level. Accompanied by falling inflation due to the continued tight monetary policy stance, we expect household expectations to maintain a gradual improvement. Maintaining effective communication with all sectors of the economy during this process remains crucial for the steady continuation of the improvement in expectations.

[1] D’Acunto, F., De Fiore, F., Sandri, D., & Weber, M. (2025). A Global Survey of Household Perceptions and Expectations. BIS Quarterly Review, 33-48.

[2] Weber, M., Gorodnichenko, Y., & Coibion, O. (2022). The expected, perceived, and realized inflation of US households before and during the covid-19 pandemic (No. w29640). National Bureau of Economic Research.

[3] Consumers' Perceived and Expected Inflation, CBRT Inflation Report 2024-IV, Box 3.1

[4] D’Acunto, F., Charalambakis, E., Georgarakos, D., Kenny, G., Meyer, J., & Weber, M. (2024). Household inflation expectations: An overview of recent insights for monetary policy.

[5] D’Acunto vd. (2025).