The impact of monetary policy on the real economy becomes visible via the transmission mechanism. Therefore, the channels through which monetary policy decisions affect the economy and the effectiveness of the transmission mechanism are crucial for central banks. In this scope, to assess the effectiveness of the transmission of monetary policy implementations to short-term market rates, deviation indices are employed in the literature[1]. In this blog post, we analyze the recent developments in the transmission mechanism by using the deviation index we have derived for Turkey.

Transmission to Short-Term Market Rates and the Interest Rate Deviation Index

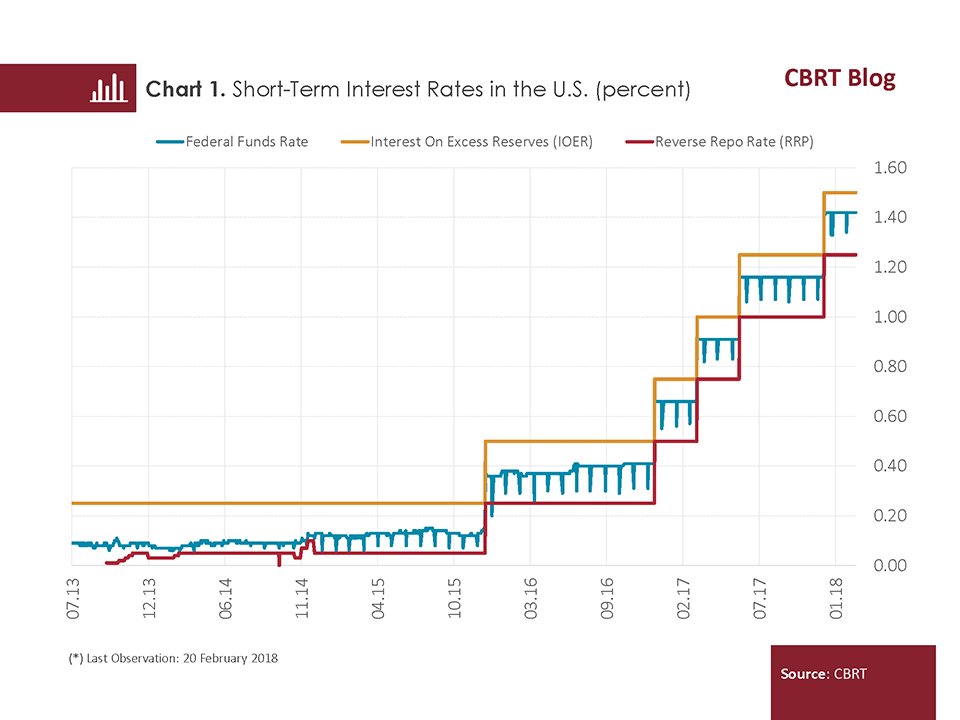

For the interest rate channel of monetary policy to work effectively, the transmission of the policy rate to short-term market rates should be strong. As a matter of fact, the transmission to short-term money market rates is the first step in the transmission to other medium- and long-term market rates (such as treasury bonds, currency swap, credit, deposit rates, etc.). Under a perfect competition structure where markets function flawlessly and all market players enjoy equal conditions with respect to market access and costs, interest rate decisions of central banks are expected to be completely passed through to money market rates adjusted for term premium and credit risk. However, in practice, the absence of perfect competition conditions, various regulations, and the divergence of market players’ (creditor/borrower) behaviors lead to deviations in the transmission of monetary policy decisions to money market rates. These deviations, which are supposed to be zero under an ideal structure of a fully effective monetary transmission, indicate a less effective transmission. For example, certain monetary policy implementations in the U.S. occasionally lead to weakened effectiveness of transmission. As government sponsored enterprises (GSEs), which hold excess reserves by definition, cannot sell these excess funds to the Fed, market rates usually remain below the interest rate paid by the Fed on excess reserves (IOER – the base level for interest rates). In 2013, with the Fed engaging more market players in the overnight reverse repo (RRP) facility, transmission to money market rates improved and the RRP rate began to form a base level for money market rates (Chart 1).

Eventually, instruments that central banks choose and the regulations they introduce may affect the degree of the pass-through of policy decisions to short-term interest rates.

Interest Rate Deviation Index and Predictability of Monetary Policy

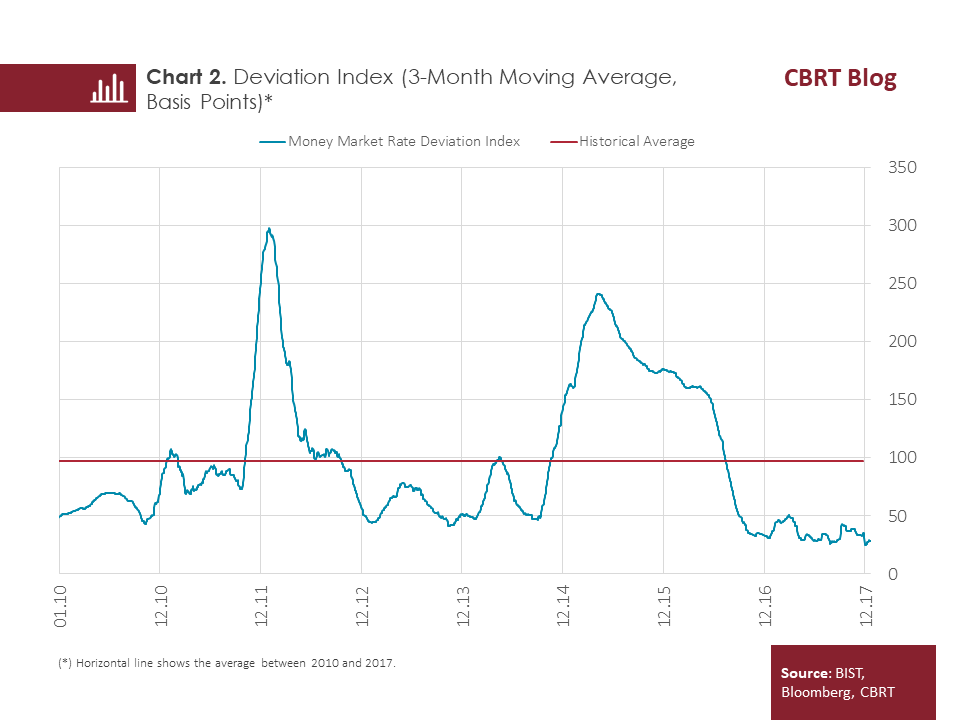

The deviation index (Money Market Rate Deviation Index) we have derived to measure the CBRT’s effectiveness on short-term market rates focuses on short-term funds that banks obtain from money markets only[2]. Taking into account their relative importance for banks’ short-term funding, one-week currency swap rates are used in addition to Borsa Istanbul (BIST) Repo/Reverse Repo Market overnight repo rates[3]. The index is calculated as the sum of the deviations of selected rates from the CBRT’s weighted average funding rate in absolute value weighted by the volume. An analysis of the changes in the Money Market Rate Deviation Index for Turkey since 2010 shows that the interest rate corridor and liquidity management (setting of the funding composition on a daily basis) practices actively used from time to time may cause deviations in short-term interest rates (Chart 2). The Money Market Rate Deviation Index has been on a downtrend since the mid-2015 due to the convergence between the CBRT’s weighted average funding rate and money market rates following the termination of the additional monetary tightening and the developments in the funding composition. In the recent period, it has fallen below the historical average as of the second half of 2016. In 2017, the Index continued to fluctuate well below its historical average on the back of the CBRT’s actions to increase predictability of the monetary policy stance and liquidity measures. As the CBRT provided funding predominantly through a single channel, effectiveness and predictability in money markets significantly increased.

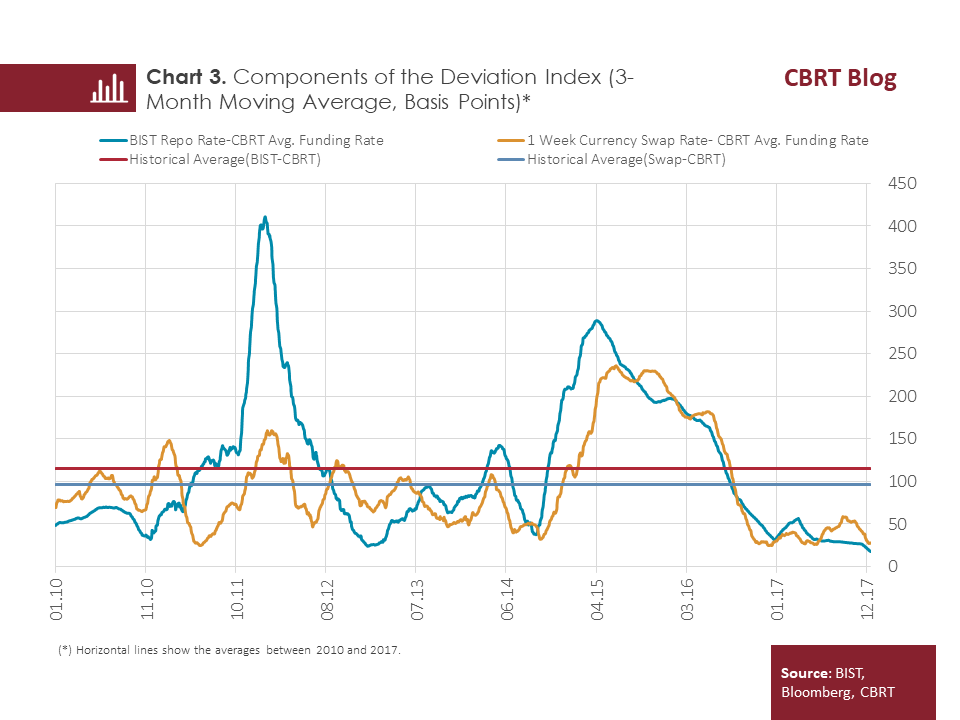

A close look at the index components (Chart 3) reveals that short-term interest rates significantly deviate from the CBRT’s weighted average funding rate in some periods due to the active use of the interest rate corridor. Foreign Exchange Deposits against TL Deposits Auctions introduced by the CBRT in early 2017 are also considered to have contributed positively to the downtrend in the deviation index by facilitating a more concerted movement of currency swap rates with other money market rates.

To sum up, the recent historically low level of the deviation index is a positive indicator of the effectiveness and predictability of monetary policy implementations.

[1] January 2018 volume of the Inflation Report includes detailed information regarding the calculation of the index (See Box 5.1). The deviation index is calculated as the sum of the deviations of money market rates, which are crucial for banks’ short-term funding, from the CBRT’s weighted average funding rate in absolute value weighted by the volume.

[2] Kara (2015) and Küçük et al. (2016) emphasize that BIST repo rates are crucial in the monetary transmission mechanism of Turkey. On the other hand, also considering banks’ borrowings from non-CBRT resources in money markets, Ünalmış (2015) includes non-CBRT BIST and currency swap market volumes and rates in the calculation of the effective funding rate. One-week currency swap rates are adjusted for term premium using USD/TRY forward implied rates, thus obtaining “overnight equivalent” of interest rates.

[3] Duffie D. and Krishmamurthy A. (2016), “Pass-through Efficiency in the Fed’s New Monetary Policy Setting“, Jackson Hole Symposium of the Federal Reserve Bank of Kansas City 2016.

Bibliography

Duffie D. and Krishmamurthy A. (2016) “Pass-through Efficiency in the Fed’s New Monetary Policy Setting“, Jackson Hole Symposium of the Federal Reserve Bank of Kansas City 2016.

Kara, H. (2015) “Interest Rate Corridor and the Monetary Policy Stance”, CBRT Research Notes in Economics, No: 2015-13.

Küçük, H., P. Özlü, A. Talaslı, D. Ünalmış and C. Yüksel (2016) “Interest Rate Corridor, Liquidity Management, and the Interest Rate Corridor”, Contemporary Economic Policy, 34(4): 746-761.

CBRT Inflation Report 2018-I, Box 5.1, “Effectiveness of the CBRT on Money Market Rates”.

Ünalmış, Deren (2015) ”Interest Rate Corridor, Liquidity Management and the Effective Funding Rate in Money Markets” (in Turkish), CBRT Research Notes in Economics, No: 2015-20.