In fresh fruit and vegetable trade in Turkey, there are a number of middlemen between the producer and the end consumer such as tradesmen outside the market hall, brokers and tradesmen operating in the wholesale market, forwarders and retailers. The number of farmers conducting their production and marketing activities within the body of organized structures is small and the existing producer organizations are not active enough in production and marketing processes. The majority of the marketing functions such as the supply, transport, storage, packaging and classification of fresh fruits and vegetables is performed by middlemen. This situation increases the dependency of producers on middlemen on the one hand, and elongates the marketing channels, elevates costs and raises the marketing share on the other hand. Therefore, ensuring efficiency in post-production supply processes is as critical as boosting productivity for a healthy price formation in fresh fruit-vegetable products.

This study presents an exemplary numerical exercise based on an extended supply chain and a step-by-step evaluation of the price formation in the chain. In addition, the study sheds light on the taxation dimension of the fresh fruit-vegetable supply chain and offers suggestions for increasing the efficiency of the supply chain as well as for a healthier price formation.

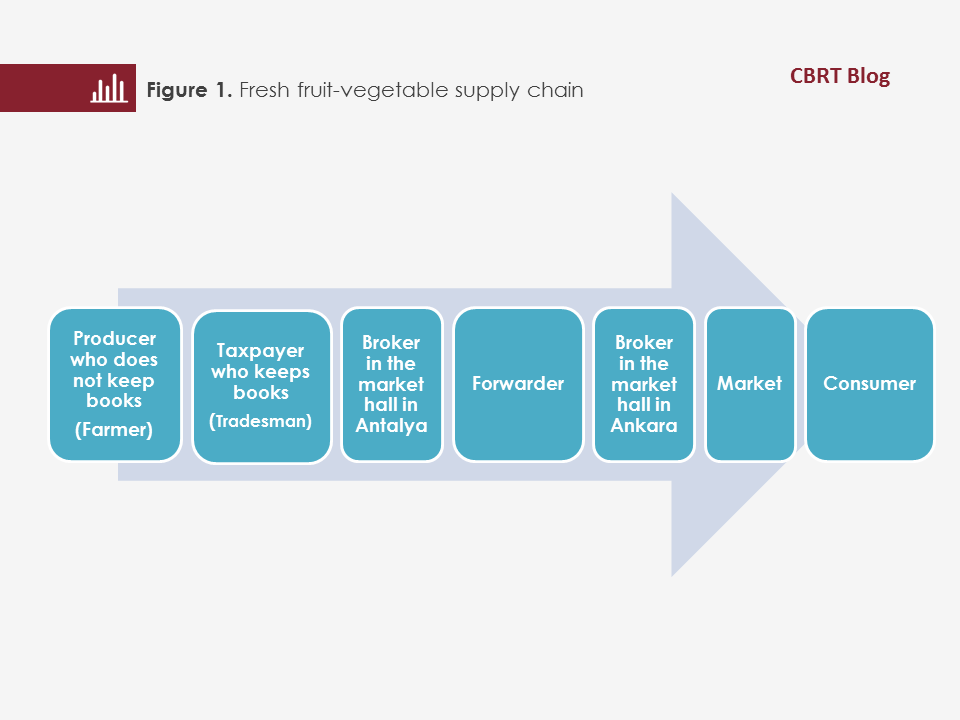

I- Fresh fruit-vegetable supply chain

The exercise is based on an example in which a certain amount of vegetables that a farmer from Antalya has harvested reaches an end consumer in Ankara via middlemen. The supply chain forming the basis of our exercise is shown in Figure 1.

Through a numerical exercise based on various loss, amount and price assumptions, we will analyze the price formation and the value share in the fresh fruit-vegetable supply chain.

In the first step of the supply chain, the taxpayer who keeps books (tradesman) buys from the producer who does not keep books (farmer) 10,000 kilograms of tomatoes at a price of 1 TL per kilogram. After deducting the 2-percent income tax withholding and the 1-percent BAĞ-KUR (the pension fund for the self-employed in Turkey) cut to be paid to the relevant public authorities on behalf of the farmer, the tradesman will pay him the remaining amount.[1]

In the second step, the tradesman sells the tomatoes to the forwarder at a price of 1.3 TL per kilogram (VAT excluded) via the broker in the market hall in Antalya. We can define the broker as a real or legal person who sells the product in the wholesale market hall in return for commission. The forwarder is a real or legal person who sends the product he bought from the broker to brokers in other wholesale market halls to be sold in return for commission. The broker invoices both the tradesman and the forwarder. The invoice that the broker issues for the forwarder includes the product’s price, the market hall charges calculated as 1 percent on this price and the VAT calculated as 1 percent on the total amount. The market hall charges refer to the amount paid by the buyers of the products to municipalities or businesses having a wholesale market hall, calculated on the total sale amount.[2] Additionally, the broker calculates an 8-percent commission charge on the sale amount and 18-percent commission VAT on this commission charge, and collects these amounts from the forwarder.[3]

In the third step, we assume that the forwarder makes a deal with the broker in the market hall in Ankara to sell the tomatoes at a price of 2 TL/kg (VAT excluded) and the broker sells the tomatoes to the market at this price. By the way, we presume that there is a 10-percent loss during the transport from Antalya to Ankara and the broker receives 9,000 kilograms of tomatoes. The forwarder will pay the broker an 8-percent commission charge on the sale amount and 18-percent commission VAT on the commission charge. We also assume that the forwarder has paid 800 TL (VAT excluded) for the transport from Antalya to Ankara. There will be an 18-percent VAT cut on the transport service to be paid to the tax administration.

In the final step, let us suppose that the market incurs a 10-percent market loss in the 9,000 kilograms of tomatoes that it purchased from the broker in the market hall and sells the remaining 8,100 kilograms of tomatoes at a price of 2.6 TL/kg (VAT excluded) to the end consumer. End consumers will pay a total of 22,744.8 TL (the 8-percent VAT included) for 8,100 kilograms of tomatoes.

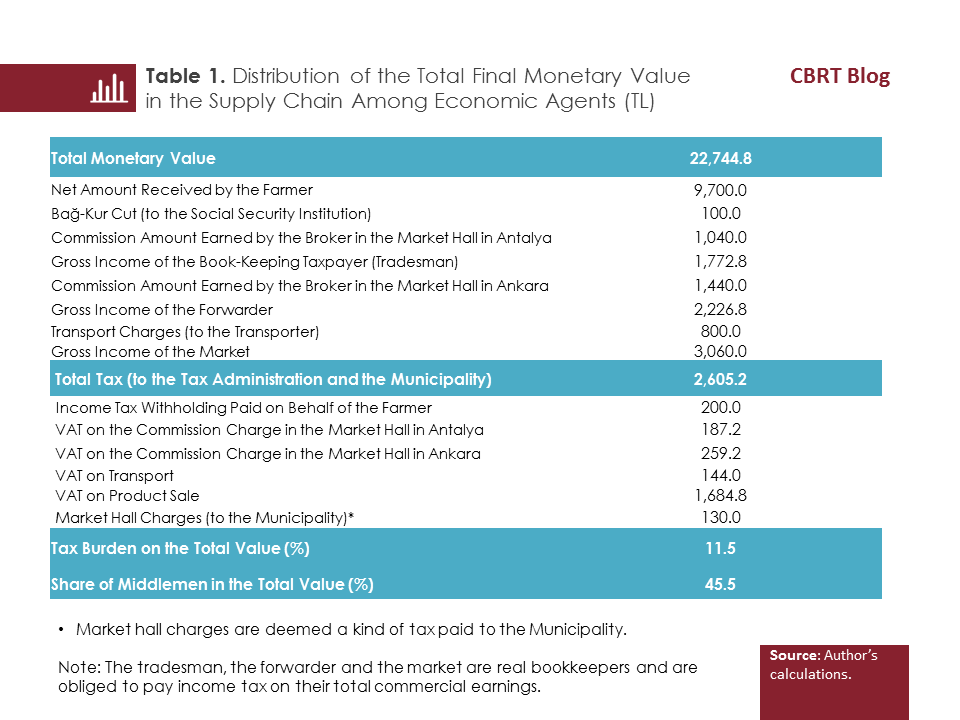

In our example, the product in the farm reached the end consumer through a long supply chain. The tomatoes left the farm at 10,000 kilograms, diminished to 8,100 kilograms due to losses on the road and in the market, finally reached a monetary value of 22,744.8 TL, and were consumed at a price of 2.81 TL/kg (VAT included). Table 1 shows how this monetary value is shared among various economic agents in the supply chain.

It is noteworthy that the share of middlemen in the total value is 45 percent. Available data show that this share may be higher depending on the product and the period. Moreover, it is known that the loss rates periodically exceed the assumptions in the analysis and reach 50 percent in certain products.

II- Tax Analysis

Of the total monetary value of 22,744.8 TL, 11.5 percent goes to the relevant public administration as tax. It should also be noted that the middlemen in the chain such as the tradesman, the forwarder and the market are obliged to pay an income tax on the net commercial earnings they obtain from their total commercial activities.

A detailed analysis of the tax cuts in the supply chain suggests that:

1- The 2-percent income tax withholding cut on behalf of the farmer is reasonable and does not have a significant effect on the final price.

2- There is an 18-percent VAT cut on commission and transport charges. Although the VAT on commission is cut over the commission charge, in practice, the brokers reflect the commission VAT amounts to the economic agents such as farmers, tradesmen and forwarders for whom they act as middlemen for the selling of the product. Likewise, the transporter also reflects the VAT on transport to the forwarder. Accordingly, these VAT rates turn into a cost factor for those selling their products in the chain, and are reflected to the prices asked and consequently to the final consumer price.

3- The VAT on fresh fruit-vegetable sales is applied at a rate of 8 percent over the final consumer price. The VAT amounts cut on the product sales in the intermediate stages of the supply chain are netted through settlement and the total VAT on product sales paid to the tax administration throughout the chain realizes at 8 percent over the final consumer price.

III- Policy recommendations

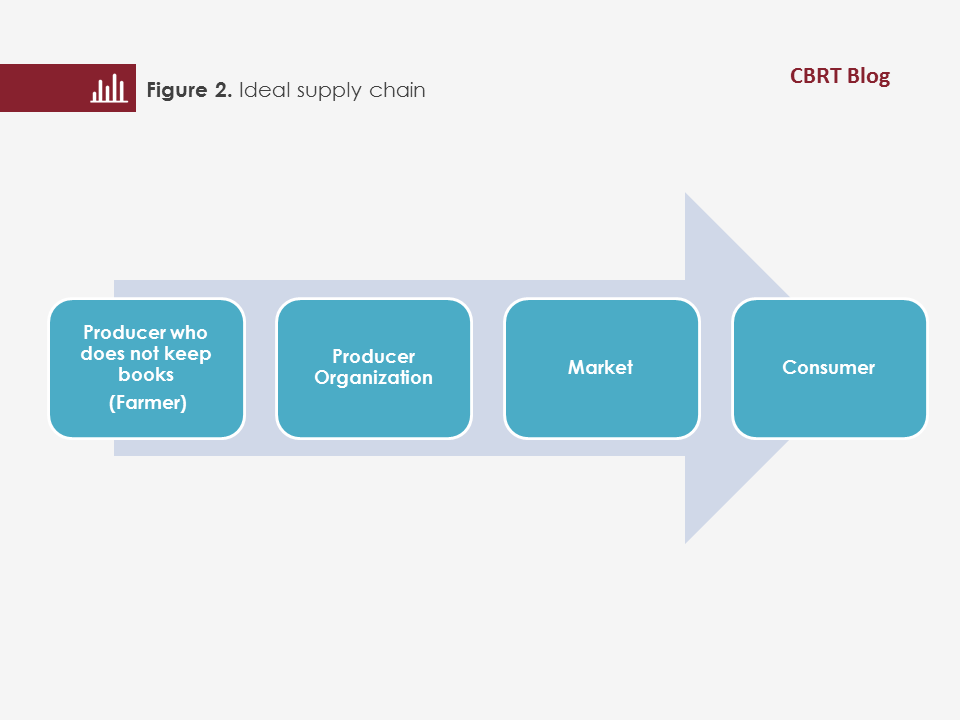

1- Figure 2 offers a supply chain example believed to be the “ideal” one, in which the product of the farmer reaches the market and then the consumer via a producer organization.

It is widely known that the producers in the fresh fruit-vegetable sector in Turkey produce on a small scale and cannot perform production and marketing activities via organized structures. Hence, rather than a supply chain that we define as ideal, there emerges a structure that involves a number of middlemen who all take a share from the final price. In this context, it is of critical importance that the producer organizations are empowered and encouraged.

Introducing additional tax advantages for the commercial transactions that the producer organizations are engaged in will be instrumental in establishing producer organizations, increasing the number of their members and thus making the ideal fresh fruit-vegetable supply chain widespread. Moreover, there will be a downward effect on the prices of fresh fruits and vegetables which will meet the markets and then the end consumer via an ideal supply chain, as the number of middlemen in the supply chain will be minimized.

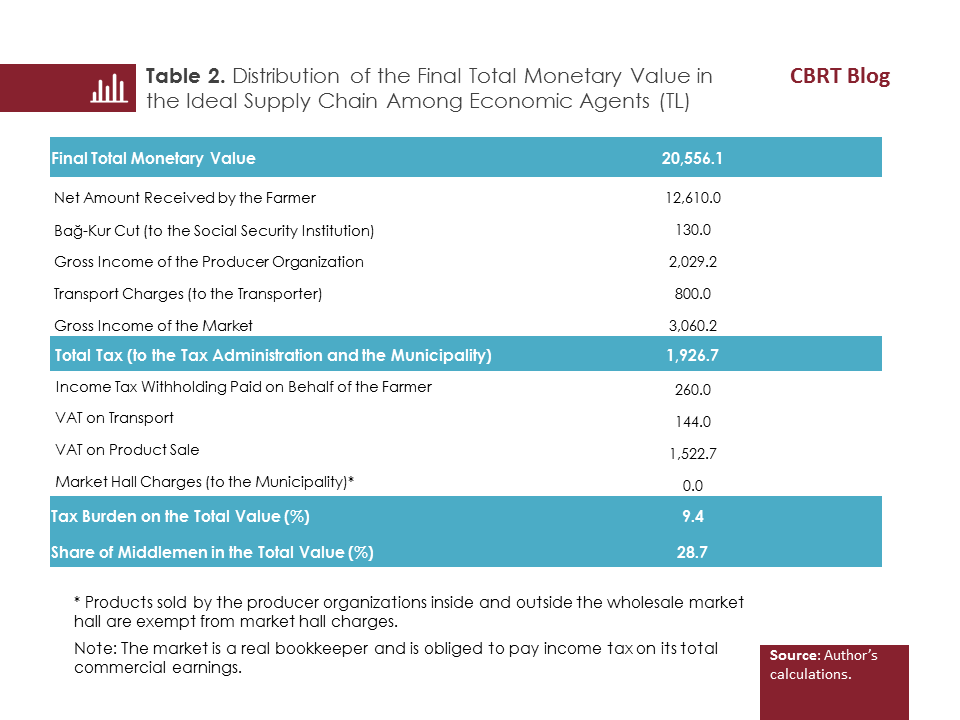

To see the extent of the effect on the final consumer price if the fresh fruit-vegetable supply chain occurs in the ideal structure shown in Figure 2, we have replicated our previous numerical exercise for the ideal supply chain without changing the amount, transport charge and loss rate assumptions. We assumed that the farmer sells 10,000 kilograms of tomatoes to the producer organization at a price of 1.3 TL/kg (VAT included), the producer organization sells 9,000 kilograms of tomatoes to the market at a price of 1.79/kg (VAT included), and the market sells 8,100 kilograms of tomatoes to the end consumer at a price of 2.54 TL/kg (VAT included). Also, we presumed a price setup in which the market’s gross income remains the same as in the first exercise. The distribution of the total monetary value of 20,556.1 TL attained in the ideal supply chain among the economic agents is shown in Table 2. In the ideal supply chain exercise, the consumer price materializes at 2.54 TL instead of 2.81 TL in the first exercise. In addition, the tax burden on the total monetary value drops from 11.5 percent to 9.4 percent, while the share of middlemen declines from 45.5 percent to 28.7 percent. On the other hand, the share that the producer takes from the total monetary value increases as much as 50 percent. Reducing the loss rates through improvements to be made in logistics processes may further accentuate the price effects.

2- According to the legislation, the commission rate that the brokers charge over the selling price is freely determined by the parties provided that it does not exceed 8 percent. Moreover, the relevant Ministry is authorized to reduce this rate by half. Information gathered from the field show that the commission rate is applied at the ceiling rate of 8 percent. In this context, slightly reducing this ceiling rate is an option that may create a positive impact on the pricing in the supply chain. For example, let us assume that the brokers in the market halls in Antalya and Ankara charge a commission at a rate of 4 percent instead of 8 percent in the supply chain in Figure 1. We replicate our numerical exercise based on the new commission rate. In this case, we see that the final consumer price decreases by 4.83 percent under the assumption that the gross incomes of the tradesman, the forwarder and the market in the intermediary steps of the supply chain remain unchanged.

To conclude, analyses regarding the fruit-vegetable markets, which constitute one of the most important items in terms of the food inflation, reveal that the following three issues are critical for a healthy price formation: creating an effective supply chain that will minimize the share of middlemen, designing the taxation model in a way to encourage the producer organizations and diminish the number of middlemen, and improving the logistics processes so that the loss rates are reduced. The results that the steps taken by the Food Committee will produce concerning these issues are believed to trigger a permanent increase in productivity as well.

[1] Pursuant to article 94, subparagraph 11 of the Income Tax Law, the income tax withholding is applied at 2 percent for agricultural products bought by registering them in commodity exchanges, and at 4 percent for agricultural products bought without registering.

[2] Regulation on Vegetable and Fruit Trade and Wholesale Market Halls, Article 44/1: Of the products imported in the framework of the related legislation and the products purchased from the producers against invoices or producer receipts, those sold in the wholesale market hall are subject to 1-percent market hall charges and those sold outside the wholesale market are subject to 2-percent market hall charges.

[3] Regulation on Vegetable and Fruit Trade and Wholesale Market Halls, Article 35/1: The commission rate that the brokers charges over the selling price is freely determined by the parties provided that it does not exceed 8 percent. The relevant Ministry is authorized to reduce this rate by half.